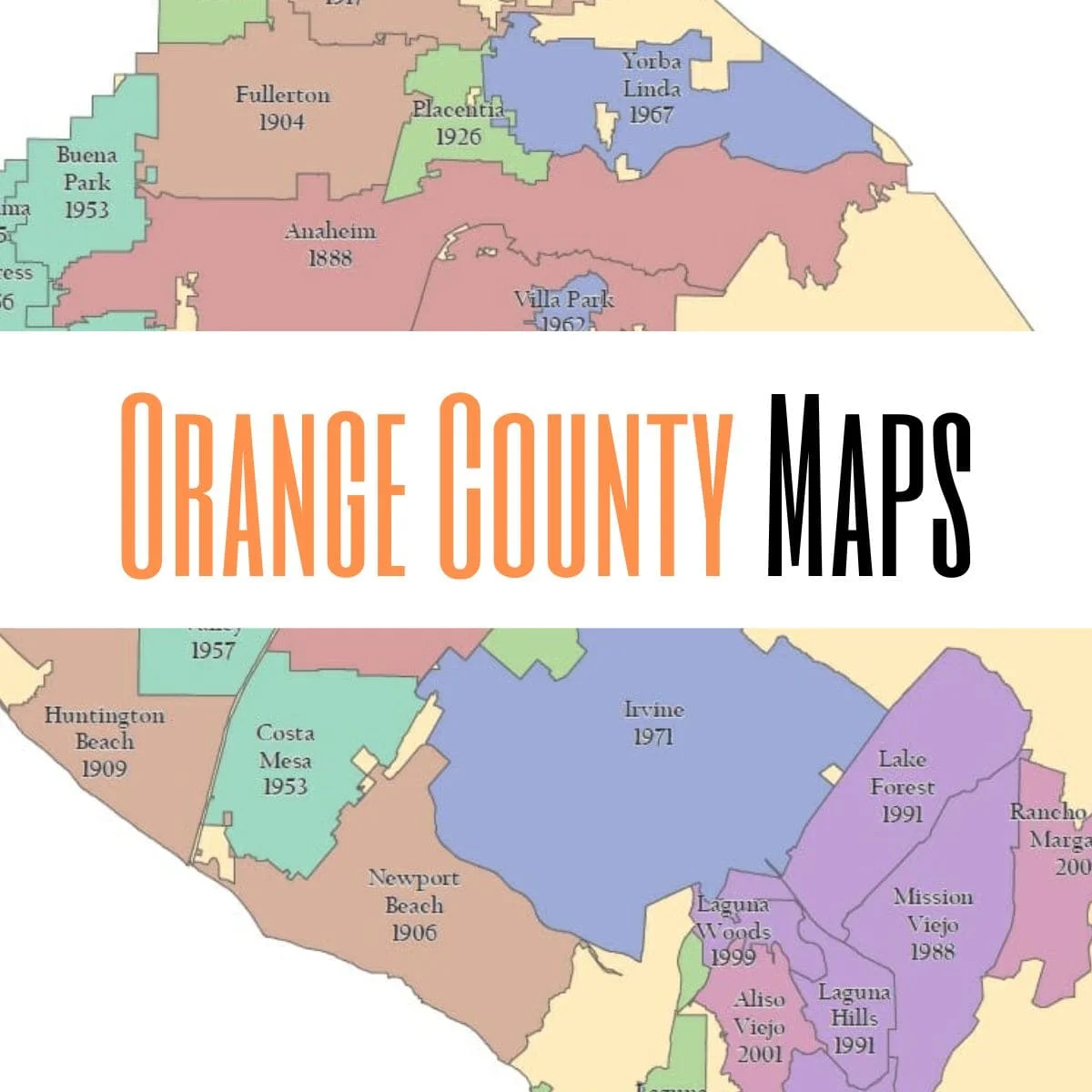

Find information, tools and resources about Real Estate in Orange County, California. From the most the most luxurious to affordable cities we've got you covered.